[ad_1]

With the calendar silent and seemingly fifty percent the Town on the ski slopes, how could FT Alphaville not be intrigued by evaluation that mentions a “death zone”?

Morgan Stanley has seized upon the week’s alpine overtones with some mountain-themed fairness approach, with some fascinating takeaways on the dash to trash we’ve seen so far in 2023.

Michael Wilson and buddies have their eyes on fairness danger premium — they warn that this gauge of potential upside has plunged to its most affordable degrees in the article-money-disaster era:

With the Equity Possibility High quality at its most affordable degree because 2007, the possibility-reward for shares is very lousy, specially with a Fed that is possible considerably from carried out, and earnings anticipations that are 10-20% also substantial. It is time to head back again to foundation camp before the future guideline down in earnings.

They reckon:

— Robust the latest knowledge has “taken a Fed pause/pivot totally off the table”

— In spite of bearish vibes, “both energetic institutional and retail investors are extra bullish than they have been in around a year”

— Earnings per share expansion and sales progress have become disconnected, which usually means an EPS slowdown looms

The recent equity rally has been fuelled by a stunning abundance of liquidity, even as the Federal Reserve moves to tighten financial policy. Somewhat than preventing (or not fighting) the Fed, traders should really choose a a lot more world wide look at, claims Morgan Stanley:

[We] believe the major reason for why shares have been rallying due to the fact Oct has to do with the abundant world liquidity that has been delivered from the PBoC, BOJ and weaker USD relatively than any dovish transform from the Fed . . .

[We] imagine the “offset” from the PBoC, BOJ and weaker dollar has much more than cancelled out the Fed’s exertion to tighten economic problems which have loosened noticeably from Oct degrees.

They proceed:

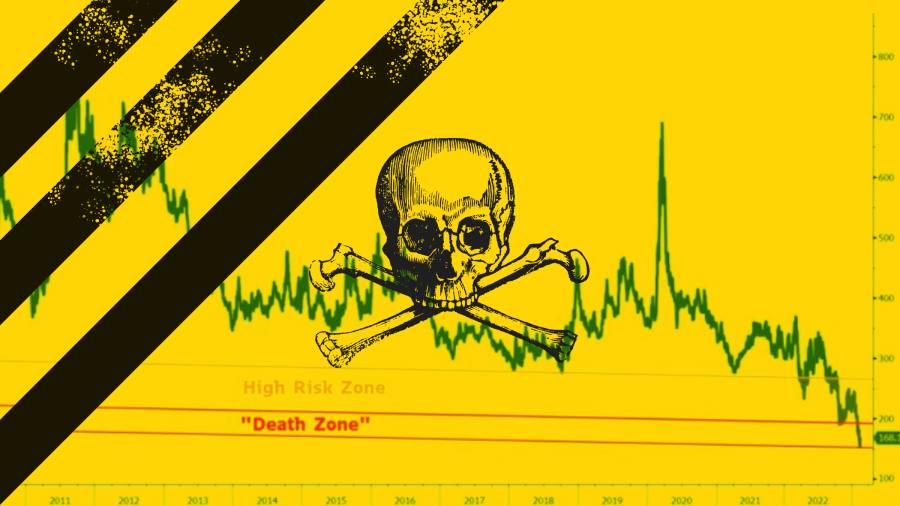

The inconsistency of the price tag motion concerning stocks and bonds is a superior case in point of wrong readings through a time when liquidity may perhaps be clouding the essential image. Most likely the strongest proof that the latest natural environment is just one of the riskiest we have witnessed because this bear industry started comes from the most up-to-date looking through of our Equity Possibility Premium . . .

With the ERP achieving just 155bps very last 7 days, we consider the threats are extraordinary now and nearly extremely hard to justify with any narrative 1 needs to conjure up.

Here’s that ERP “death zone” in all its glory. (Should not the peaks be more perilous in a mountain analogy? Winter athletics fanatics please comment below.)

The strategists say the current rally is a perilous illusion, with the risk-reward on the S&P 500 now “very poor”:

This is pure FOMO at its best, in our check out, and we come across all the hoopla and enjoyment about the YTD rally to be misplaced. The reality is that the S&P 500 is flat above the earlier 11 months and precisely in line with where by we took off our tactical bullish phone on December 5th at 4,071. The most important distinction is that stocks are now noticeably more pricey with the ERP at 168bps as opposed to 216bps back then.

They conclude, ominously:

Bottom line, investors are not bearish any lengthier, and this is just one more explanation to be cautious of the set-up going into what is probable to be yet another weak earnings period.

Continue to be risk-free out there, skiers.

[ad_2]

Source website link